On Superannuation Guarantee

This article was originally published by Financial Standard on 25 July 2019.

Australia’s superannuation guarantee policy is popular, economically prudent, and coming under increasing political scrutiny. It has been very effective in extending coverage of the superannuation system beyond the public sector and senior management of large companies to most working Australians. It is also seeing that increasing numbers of Australians have an independent, more comfortable retirement while reducing the fiscal policy pressures presented by an ageing population.

Even so, a small number of loud voices increasingly question whether the legislated increases in the superannuation guarantee will benefit working Australians. The Grattan Institute has argued that increasing the SG rate by 2.5 percentage points to 12 per cent will cost workers $20 billion a year in forgone wages.

Australia has been a world leader with its progressive policy and has been applauded globally. It’s popular domestically, with polling by the Association of Superannuation Funds of Australia (ASFA) indicating that over 90% of Australians support the legislated increase of SG from 9.5% to 12% in 2025. However history is littered with instances of popular policies which haven’t necessarily benefited those with whom the policy is popular.

The popularity of the superannuation guarantee should not make it immune from criticism and debate, particularly given the broad economic significance of the policy. Tellingly, the Treasurer announced that government would commission a review of the retirement income system before there is any further increase. It is a classic case of balancing individual liberties with a paternalistic state intervention.

Ensuring that the superannuation guarantee is working for those for need it most is the right thing to do, provided the discussion and analysis is grounded in fact, and not driven by ideology. Grasping the nuance of how the superannuation guarantee actually works is essential if we’re to have an informed debate.

The nuts and bolts of SG

The broad coverage of Australia’s superannuation system is an important objective. The superannuation guarantee has been effective in extending coverage to about 90% of the Australian workforce. Contrary to popular understanding however, there is no legal obligation in requiring employers to contribute to an employees superannuation fund. SG has been effective in extending coverage through the smart use of tax incentives to nudge employers to contribute.

The Superannuation Guarantee (Administration) Act does however place an obligation on employers to pay the superannuation guarantee charge to the Commissioner of Taxation of the superannuation guarantee shortfall amount.

The shortfall is the difference between the statute defined contribution rate on an eligible employee’s salary (currently 9.5%) and the amount which has been contributed for the benefit of the employee to a complying superannuation fund. In practice, these provisions do operate to require employers to contribute to a complying superannuation fund or to be required to pay an increased amount of superannuation guarantee charge.

This legal quirk of the "mandatory" Australian superannuation guarantee exists to navigate tricky Constitutional issues to ensure coverage of the superannuation system beyond employees of corporations and to partnerships and state owned employers. This was done by relying on the Commonwealth's taxation powers to legislate rather than the industrial relations of pensions powers.

Ensuring that coverage remains high or is improved will require consideration of how the superannuation guarantee can be extended to dependent non-employment work arrangements. The increase in independent contractors and sole director companies presents a challenge which may require attention in the near future to encourage participation in the gig economy through smart use of tax incentives.

Working Australia

Does more super. mean less take home salary? This question lies at the heart of debates over whether the rate of mandatory superannuation contributions should be increased to 12% on top of salary. The truth, like so many simple assertions is that it depends. It depends on how wages are set, the frequency and regularity of determining employment arrangements, and the wording of individual and collective employment contracts.

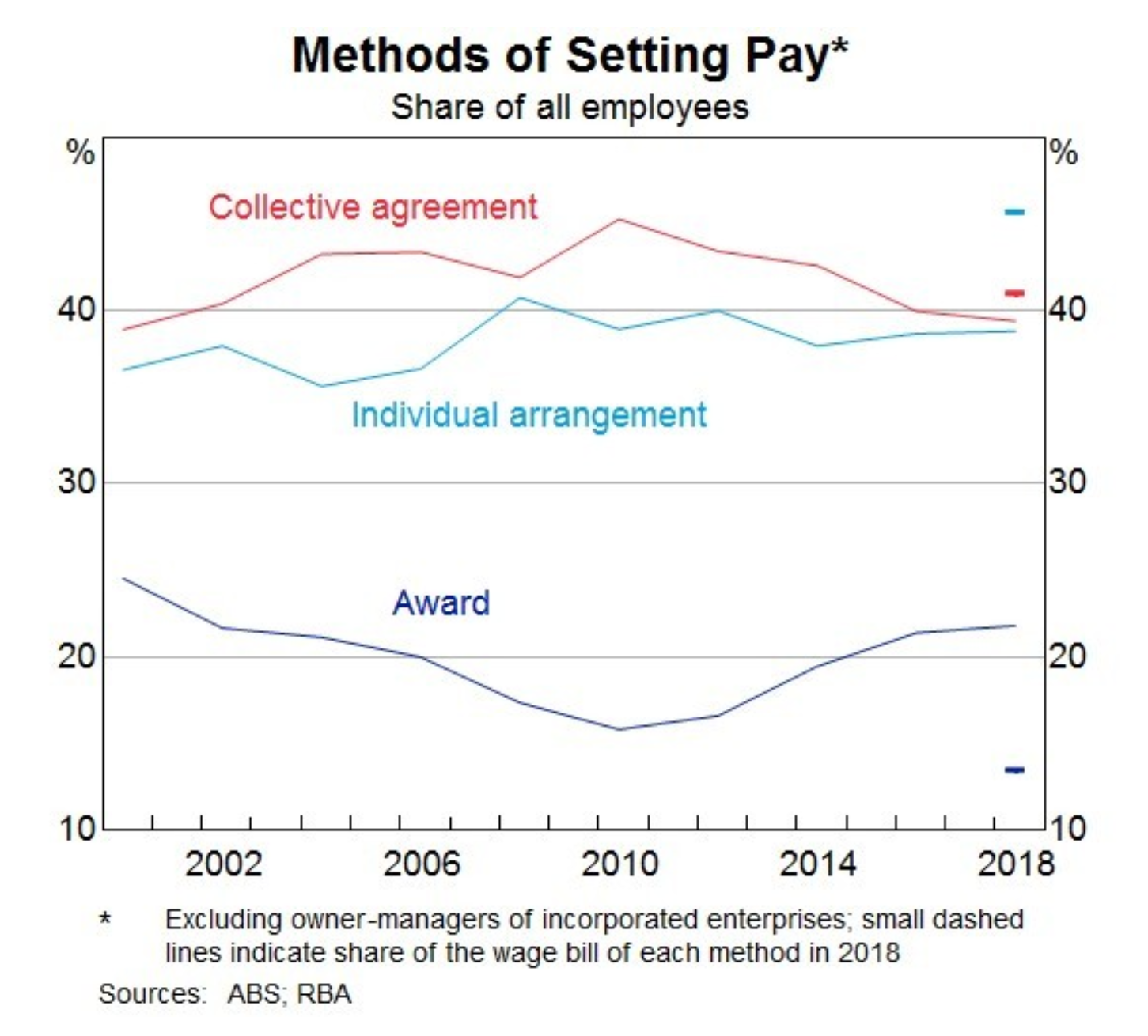

For the majority of Australians being paid above the minimum protections in modern awards (that’s about 4 in 5 workers), an increase in the SG could result in a decrease in take home wage, depending on the wording of their individual employment contract or collective agreement.

There has been a trend towards employment contracts setting a total remuneration package, which includes mandatory superannuation contributions. This means that an increase in the level of mandatory superannuation contributions could result in a reduction in salary for the 37% of typically higher waged employees on individual employment agreements.

Data on the wording of such contracts is elusive, however it is reasonable to assume that about half of the 37% of Australians employed under an individual agreement have their wages defined as a total remuneration package which would result in a reduced salary if there were an increase in SG. While all workers employed under an individual agreement are being paid above minimum wages, not all are highly paid.

The 40% of Australian workers under collective employment agreements are far less likely to include a total remuneration package which includes mandatory superannuation contributions. The complexities of collective bargaining make it less frequent and more structured a process.

This has contributed towards such collective agreements being more resilient to wording which would see a total remuneration package include employer superannuation contributions. Collective employment agreements typically agreed a level of superannuation contributions in addition to wages. There may however be some collective agreements which rely on a total remuneration package, however the majority do not.

So it’s clear that an increase in the SG rate might result in a direct reduction in take home wages for some, the majority of Australians working under a collective or individual agreement would be unlikely to see a reduction in take home salary. However there’s more to it. Consideration also need to be given to the impact on economic conditions affecting future salary increases and new agreements.

Efficiency boost?

So, there are plenty of workers on individual or collective agreements who would not see a direct reduction in their take home wages if the SG was to increase. An argument can however be made that the additional costs of increased employer paid SG contributions reduces the bargaining power of employees to negotiate increases in wages, mirroring the employers reduced labour price elasticity.

While there is some economic truth in this argument, it must be framed in the context that the labour market isn’t particularly efficient anyway. This is especially true in today’s Australia. The salary of employees often falls below market value, particularly where employees remain in the same role or with the same employer for a longer period. There may be pay increases, however these typically don’t keep pace with the market.

The Governor of the Reserve Bank of Australia recently urged employees to press for greater wage increases in response to lower than expected wage growth. This reflected the central bank’s view that there was excess elasticity in the labour market for increased labour costs without having a material impact of levels of unemployment or underemployment.

An increase in the superannuation guarantee is a blunt but effective mechanism to force improvements in labour market efficiency in times of low unemployment and wage growth - times such as those we are currently experiencing. Former Prime Minister Paul Keating, one of the leading architects on the SG introduction has repeatedly emphasised this point.

Doing it tough?

Young Australians early in their careers and workers in lower paid industries often face the most pressing cost of living challenges. It is these Australians who would benefit most from increased savings without a direct impact on their take home salary. It is also these Australians who would benefit the most from increases in take home salary today to help meet increasing living costs.

Young and lower income earners often don’t have their salaries set by the market anyway. There are still over 23% of working Australians whose salaries are determined by the Fair Work Commission in Modern Awards. The market plays a role in how these rates are set, however this is balanced against other factors by the Fair Work Commission in deciding whether a change is necessary.

To make matters worse, many casual employees on monthly incomes of less than $450 are not covered by the superannuation guarantee. This is a relic from a time where manual administration of contributions was a costly exercise. Advances in technology make this carve out obsolete and a significant flaw in the coverage and effectiveness of the superannuation guarantee.

These young and low income earners are the Australians who have the most to gain from an increase in the superannuation guarantee and removal of the "$450 rule". Rather than adding to cost of living pressures by reducing take home salary - an increase in superannuation guarantee for Australian workers on lower salaries set by Modern Awards will increase the retirement savings of those who are set to benefit most.

Less jobs?

It is however important to understand that an increase in the rate of SG would represent an increase in the costs of labour generally for employees on an individual agreement which provides a total remuneration package inclusive of SG. This would include most employees covered by collective agreements and all employees on modern awards.

Where there isn’t adequate wage elasticity in the labour market for such jobs, this could potentially result in downward pressure on the hours offered to casual workers and the availability of employment and investment by business in labour intensive initiatives.

It is important that the Fair Work Commission remains attentive to these pressures when completing biannual reviews of modern awards. However, the current state of the Australian economy seems to be well suited to absorbing the costs of a gradual increase in SG for young and lower paid employees.

Should the planned increase from 9.5% to 12% proceed?

There is a strong argument that the planned increase in the superannuation guarantee will not have a direct adverse impact on the take home pay of most employees. There will however be a reduction in take home pay for some employees on individual employment agreements.

Broad assertions that the planned increase in SG will add to the cost of living pressures faced by many Australians don't really stack up to closer scrutiny. This may simply be due to misunderstanding of the complexity and nuance in the way in which the SG and labour markets function.

There is a strong argument that the planned increases in SG will benefit the Australians that need it most, those on middle and lower incomes. The planned increase is sound economic policy for most Australian workers. Yet caution is warranted to ensure that broader economic conditions and the labour market remain adequately elastic to absorb the costs of increasing the SG without placing excessive downward pressure on levels of employment.

Jonathan

Jonathan Steffanoni - Principal Consultant, Legal and Risk

ABOUT QMV

QMV provides trusted advisory, consulting and technology to Australia’s leading superannuation, insurance, banking and wealth management organisations.

Like what you see? Please subscribe to receive original QMV content!

You may also benefit from our free monthly pensions and superannuation regulatory updates.